Types of Stablecoins Explained (2026)

A practical guide to stablecoin types, how they maintain their peg, generate yield, and the risks behind each digital dollar.

Stablecoins all promise the same outcome: one token worth one dollar.

The interesting part is that stablecoins keep this promise.

- Some stablecoins hold Treasury bills in custody.

- Few liquidate onchain collateral when markets move against them.

- Others hedge derivatives positions to manage dollar exposure.

- Uniquely, a few try to sustain the peg through incentives alone.

To an end user, they may all look like dollars. However, each one is unique and behaves differently because stablecoins are not a single product category.

They are combinations of design choices: what backs the peg? How does new supply enter circulation? Who captures the yield generated by the system?

This guide breaks stablecoins down into different types, explains the mechanisms under the hood, and discusses the purpose behind the design,

What are Stablecoins?

Stablecoins are digital assets designed to maintain a stable price (usually $1) by backing their value with reserves, collateral, or other price-stabilizationin mechanisms.

They bring a stable unit of account into crypto.

In 2025 alone, stablecoins facilitated over $27 trillion in transfer volume, enabling trading, payments, savings, and liquidity across onchain markets.

However, stablecoins are not a single design pattern. Two tokens that both trade at $1 can rely on entirely different mechanisms to maintain that outcome.

To understand those differences, three questions matter:

- What backs the peg?

- How are new tokens created?

- Where does the yield come from?

This guide uses these dimensions to classify the different types of stablecoins, starting with the most fundamental one: what backs the peg.

Types of Stablecoins by Collateral / Peg Mechanism

Stablecoins do not all achieve price stability in the same way: some rely on assets held outside the blockchain, while others depend on onchain collateral, etc. The mechanism behind the peg determines what holds the price under pressure and what fails first when conditions turn.

Here are 5 major types of stablecoins based on their way of maintaining price stability:

Let’s now dive into each of these types in detail.

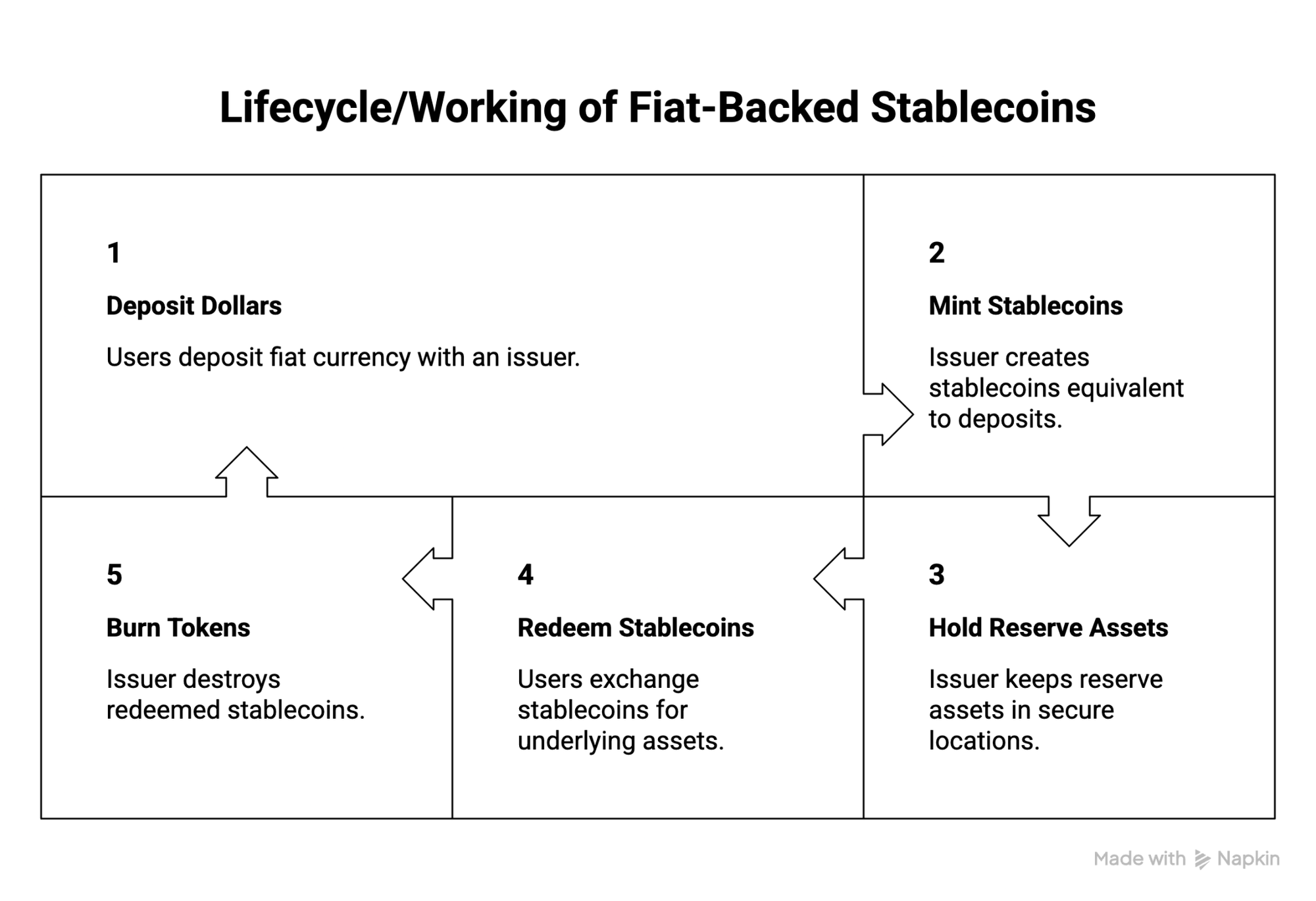

Fiat-Backed Stablecoins

Fiat-backed stablecoins are issued against cash, bank deposits, or short-duration government securities held in custody by regulated institutions.

Each token represents a direct claim on one dollar of reserves.

Popular examples of fiat-backed stablecoins are USDT and USDC.

Now, how do fiat-backed stablecoins work?

Benefits of fiat-backed stablecoins are:

- Simplest trust model: reserves are auditable, redemption path is direct.

- Deepest liquidity across CEXs, DEXs, and DeFi protocols.

- No oracle risk, no liquidation cascades, predictable behavior under normal conditions.

- Clearest regulatory path: GENIUS Act (US) and MiCA (EU) both designed around this model.

Who bears the loss?

Reserve shortfalls, banking disruptions, or redemption stress are typically absorbed by issuers and, in extreme cases, token holders who cannot redeem at par.

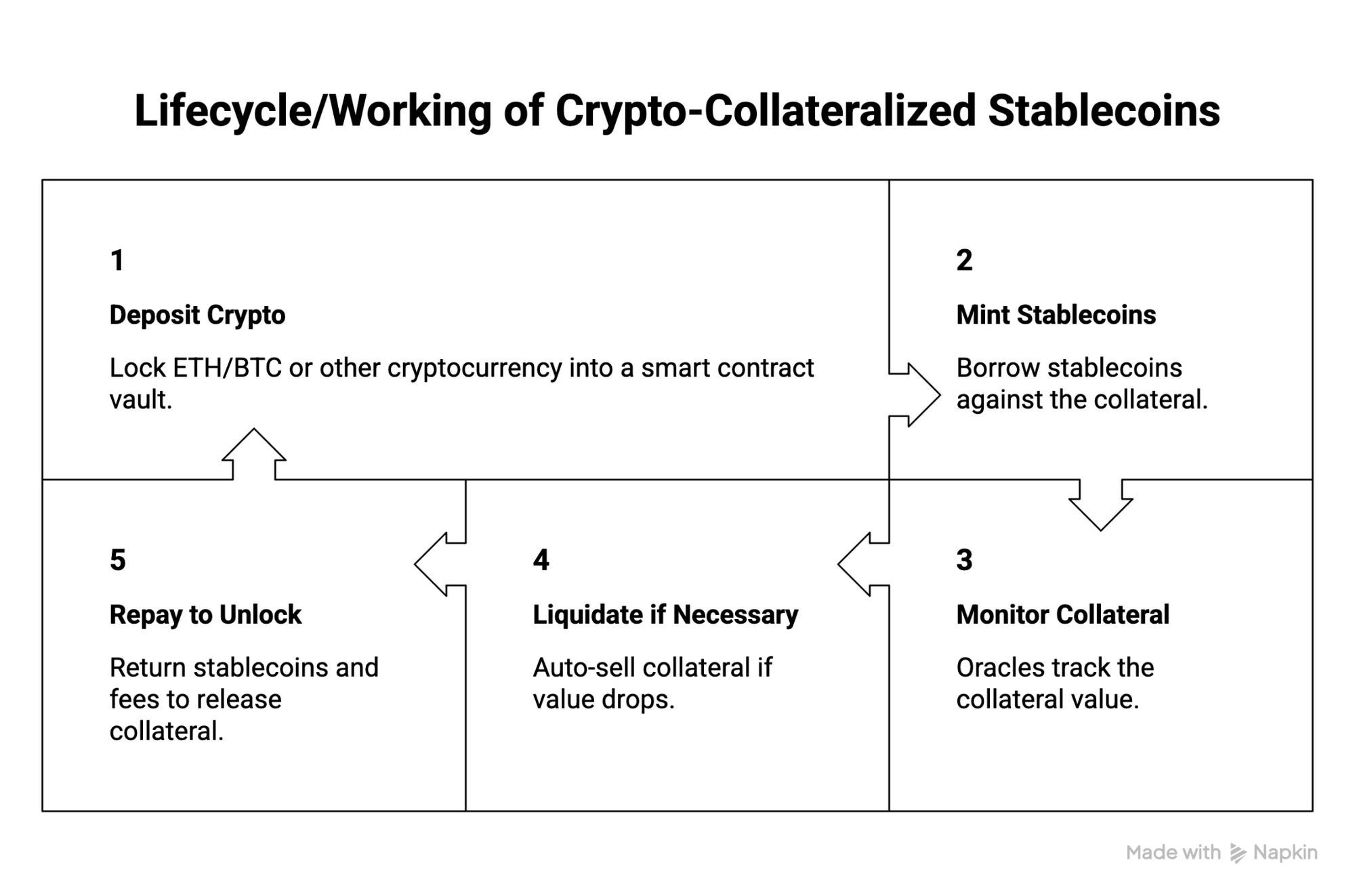

Crypto-Collateralized Stablecoins

Crypto-collateralized stablecoins are minted by locking onchain crypto assets worth more than the stablecoins issued.

The most famous example of a crypto-collateralized stablecoin is DAI.

How do these crypto-collateralized stablecoins work?

Benefits of crypto-collateralized stablecoins are:

- Issuance is permissionless and transparent.

- Reserves can be verified onchain in real time.

- Reduced reliance on banks and custodians.

Who bears the loss?

Collateral providers bear the first loss through liquidations. If liquidation systems fail during extreme market conditions, losses can propagate to the broader protocol and its users.

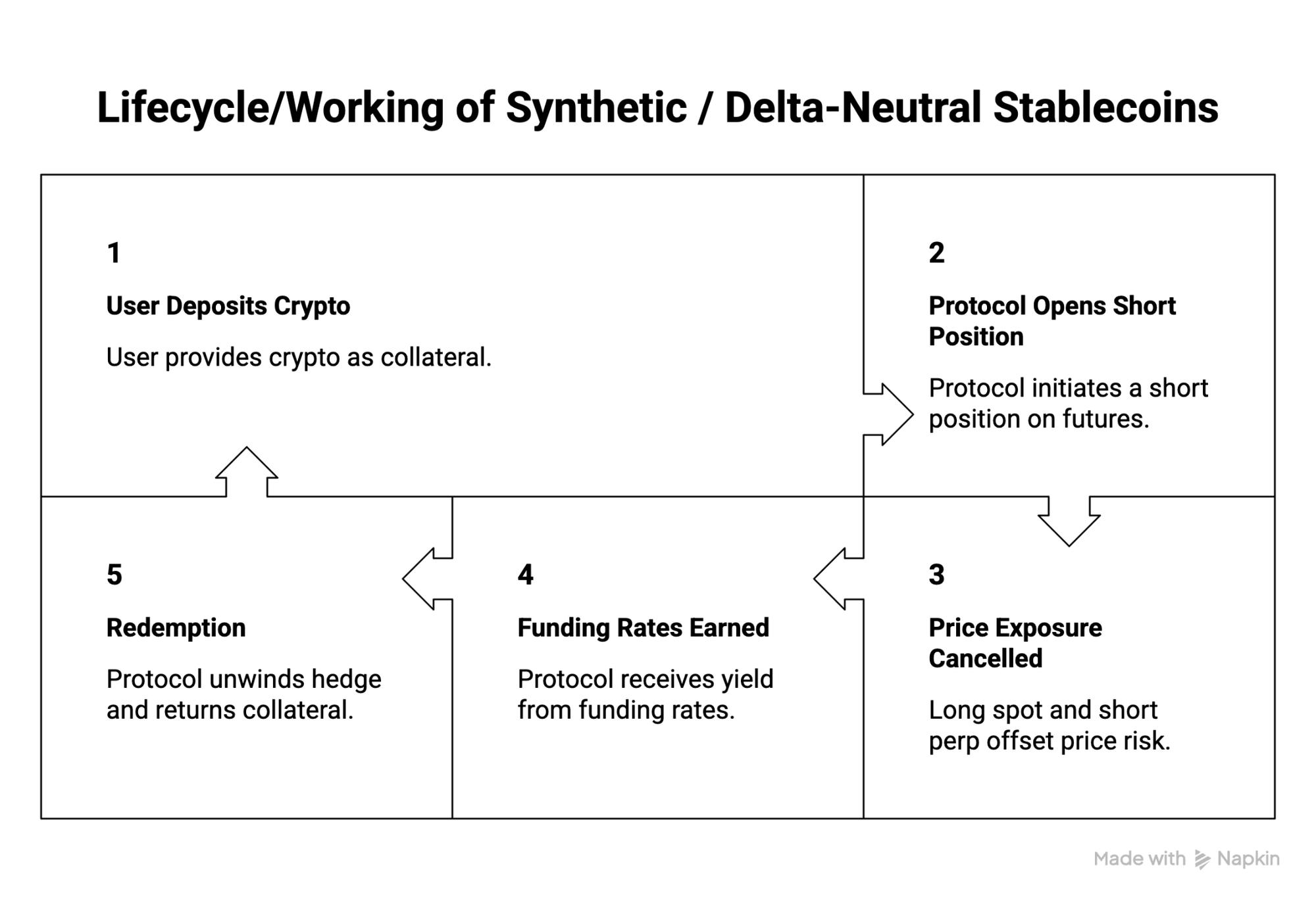

Synthetic / Delta-Neutral Stablecoins

Synthetic stablecoins maintain dollar exposure by holding crypto assets and offsetting price risk with an equal short position on perpetual futures markets. The long spot and short perp together produce a dollar-stable value without holding actual dollars.

Popular examples of synthetic stablecoins are USDe (Ethena).

How do synthetic stablecoins work?

Benefits of delta-neutral or synthetic stablecoins are:

- More capital efficient than overcollateralized models.

- Generates yield from perpetual funding rates.

- Collateral and positions are verifiable through third-party attestations.

Who bears the loss?

All protocol participants are exposed to the loss if hedges fail, exchanges become impaired, counterparties default, or funding conditions deteriorate faster than the strategy can adapt.

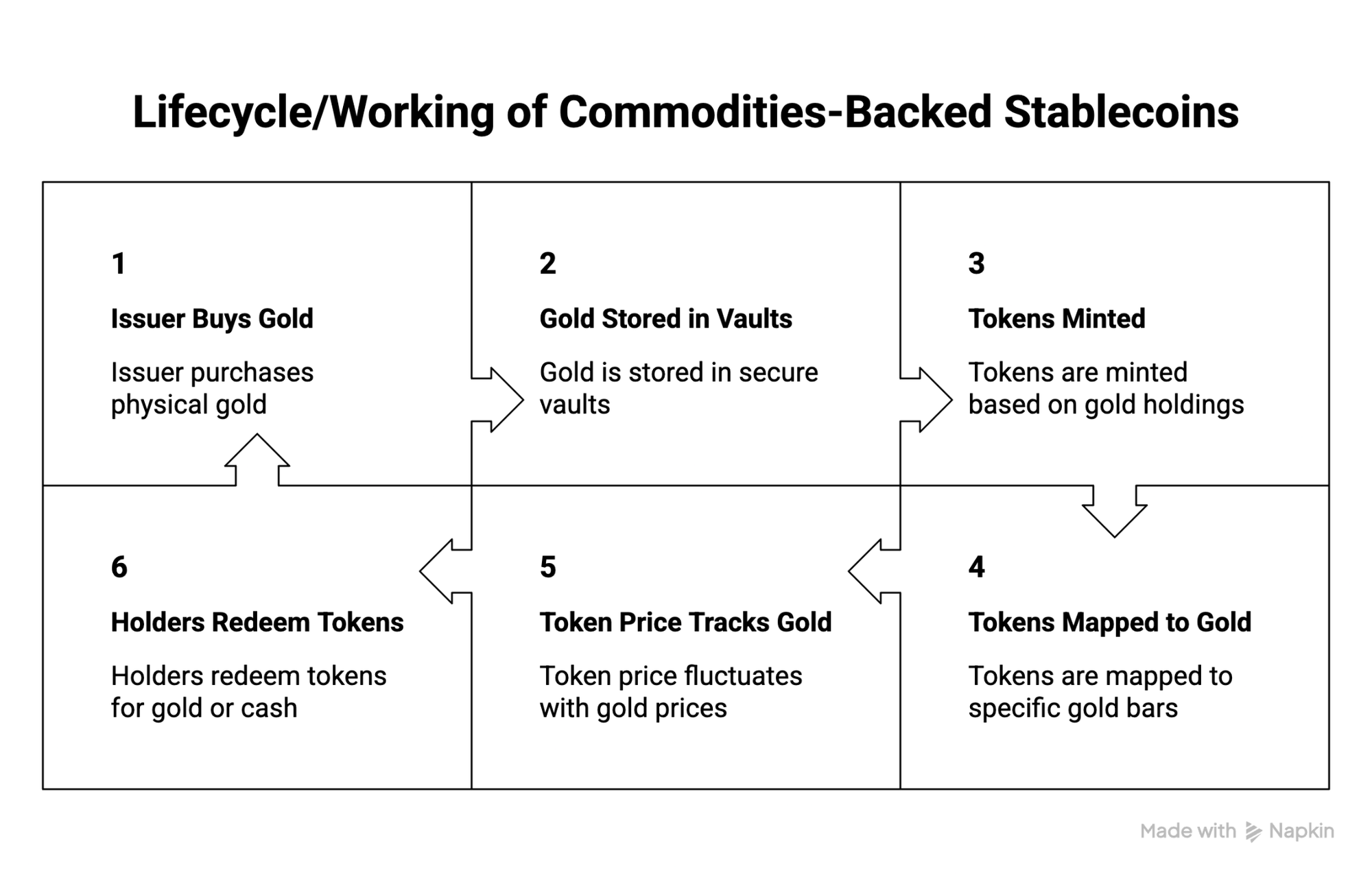

Commodity-Backed Stablecoins

Commodity-backed stablecoins are issued against physical assets held in institutional custody, most commonly allocated gold stored in audited vaults.

Each token represents ownership of a fixed quantity of the underlying commodity.

Popular examples of commodity-backed stablecoins are PAX Gold (PAXG) and Tether Gold (XAUT).

Now, how do commodity-backed stablecoins work?

Benefits of commodity-backed stablecoins are:

- Provides direct exposure to real-world hard assets onchain.

- Removes the logistical burden of storing and transporting commodities.

- Can serve as a hedge against fiat currency debasement.

- Reserve holdings can be independently verified.

Who bears the loss?

Token holders bear custodian and issuer solvency risk directly. Redemption minimums mean smaller holders cannot exit at par through the primary market and they depend entirely on secondary market liquidity.

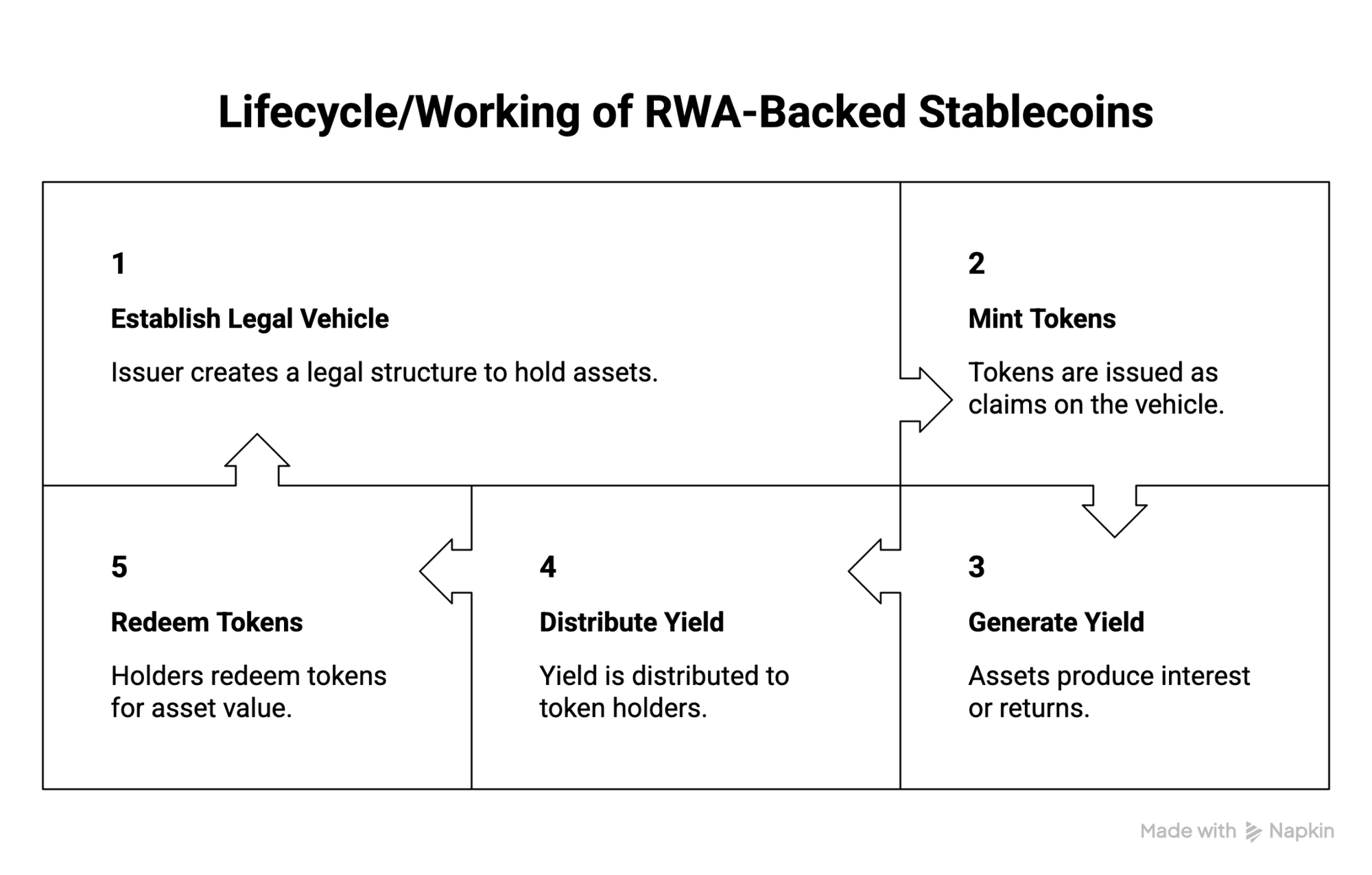

RWA-Backed Stablecoins

RWA-backed stablecoins are issued against tokenized real-world assets such as Treasury bills and money market funds. Unlike traditional fiat-backed stablecoins, a portion of the yield generated by these assets is typically passed on to token holders.

Popular examples of RWA-backed stablecoins are BlackRock BUIDL, Ondo USDY, and Ondo OUSG.

How do RWA-backed stablecoins work?

Benefits of RWA-backed stablecoins are:

- Holders earn yield from traditionally inaccessible assets like money market instruments.

- Combine the transferability of stablecoins with the income profile of short-duration fixed-income products.

- Backing assets are generally low-risk and highly liquid.

- Increasingly attractive to institutions seeking regulated onchain dollar products.

- Growing DeFi composability as protocols accept RWA tokens as collateral.

Who bears the loss?

Token holders ultimately bear losses arising from issuer failure, redemption restrictions, custody issues, or impairments in the underlying asset portfolio.

All the 5 types mentioned above are distinct in what backs the stablecoin peg. The next section deals with how new stablecoins are created/issued?

Types of Stablecoins by Issuance

Stablecoins enter circulation through one of two models: centralized issuers minting against reserves, or users minting against collateralized debt positions. The issuance model determines who controls supply creation and who has access to redemption.

The sections below explain how each issuance model works and the trade-offs they introduce.

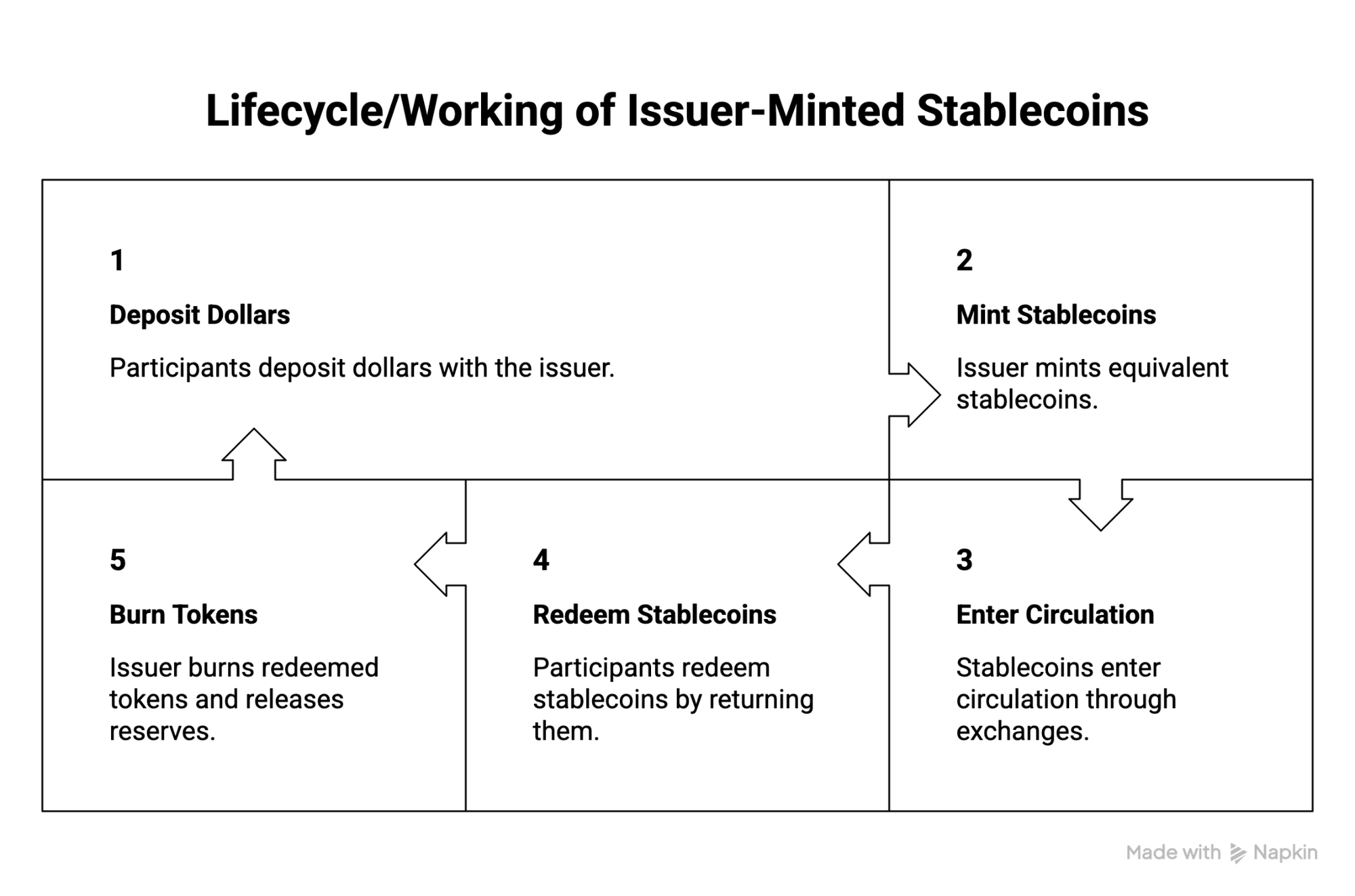

Issuer-Minted Stablecoins

Issuer-minted stablecoins are created and redeemed by centralized entities against reserve assets. While anyone can acquire these stablecoins on secondary markets, direct minting and redemption are typically restricted to authorized participants (APs).

Popular examples of issuer-minted stablecoins are USDT, USDC, and USDe.

Now, how do issuer-minted stablecoins work?

Benefits of issuer-minted stablecoins are:

- Controlled supply management, meaning the issuer has full visibility over all mint and burn activity.

- APs provide market-making depth, keeping secondary prices close to par.

- Scales to millions of users through a small number of institutional counterparties.

Who bears the loss?

Retail holders have no direct redemption path. They depend entirely on APs to maintain secondary market prices at par. If APs withdraw from market-making, retail holders absorb the depeg until redemption access is restored.

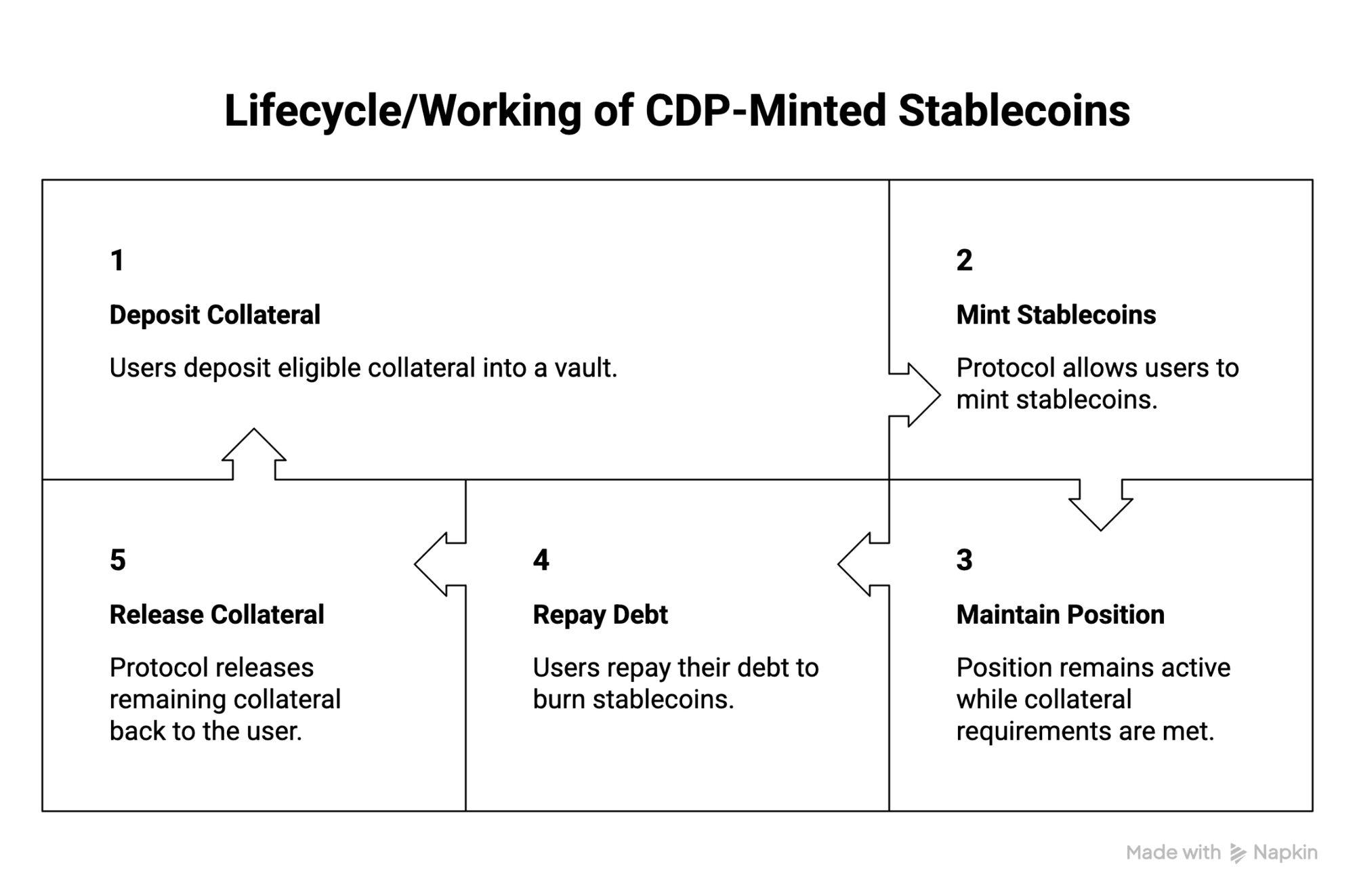

CDP-Minted Stablecoins

CDP-minted stablecoins are created when users lock collateral into smart contracts and borrow stablecoins against their positions. The stablecoin supply expands and contracts through user activity rather than a centralized issuer.

DAI is the best-known example of this model.

How do CDP-minted stablecoins work?

Benefits of CDP-minted stablecoins are:

- Permissionless: any user with collateral can mint without approval or KYC.

- Transparent and auditable supply creation.

- Supply is self-regulating, meaning stability fees rise to discourage minting, fall to encourage it.

Who bears the loss?

Vault owners bear the first loss through liquidations. If liquidations fail during extreme market conditions, losses can extend to the broader protocol and its participants.

Now, we have learned the 2 key issuance models in stablecoin design. The next section delves into stablecoins and its yield mechanisms.

Types of Stablecoins by Yield Model

Assets or strategies supporting the stablecoin generate returns. Let's understand the stablecoin types that are based on how returns are distributed.

Here’s a quick snapshot:

The sections below explain how different stablecoin designs generate and distribute yield.

Non-Yield-Bearing Stablecoins

Non-yield-bearing stablecoins maintain a fixed $1 value but pass no interest or income to holders. Reserve assets generate returns continuously but those returns accrue entirely to the issuer.

Popular examples of non-yield-bearing stablecoins are USDT and USDC.

Then, in terms of yield-bearing stablecoins, there are a few different options.

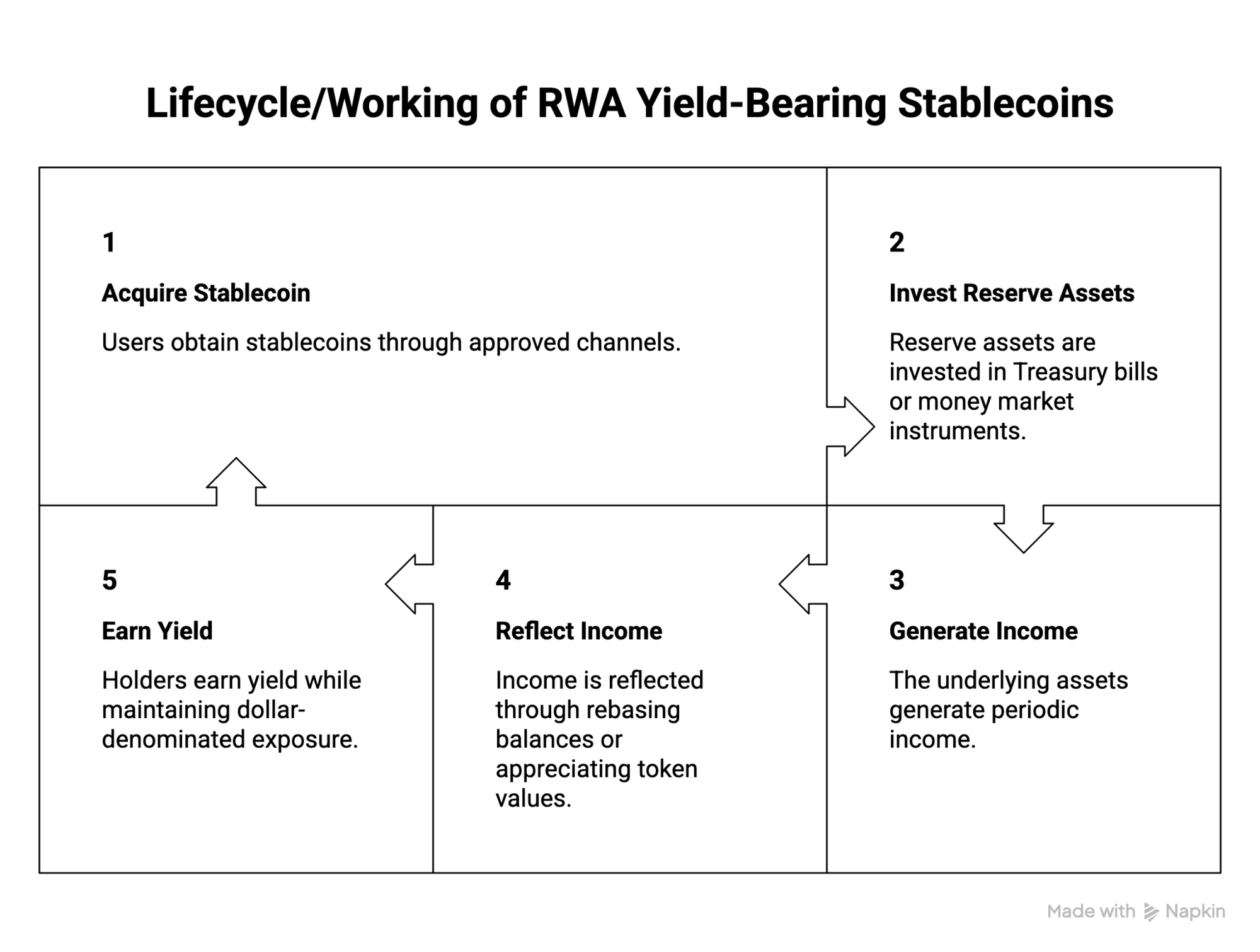

RWA Yield-Bearing Stablecoins

RWA or real-world asset-based yield-bearing stablecoins distribute income generated by underlying assets such as Treasury bills and money market funds. Instead of retaining reserve earnings, issuers pass some or all of that yield to token holders either through a rising redemption rate or an increasing token balance.

Popular examples of treasury yield-bearing stablecoins are sUSDS, USDY, and sFRAX.

How do RWA yield-bearing stablecoins work?

Benefits of treasury yield-bearing stablecoins are:

- Improves capital efficiency for idle stablecoin balances.

- Backed by the deepest, most liquid fixed income market in the world

- Growing DeFi composability: accepted as collateral across Aave, Morpho, and other protocols

- Increasingly attractive to institutions and treasuries.

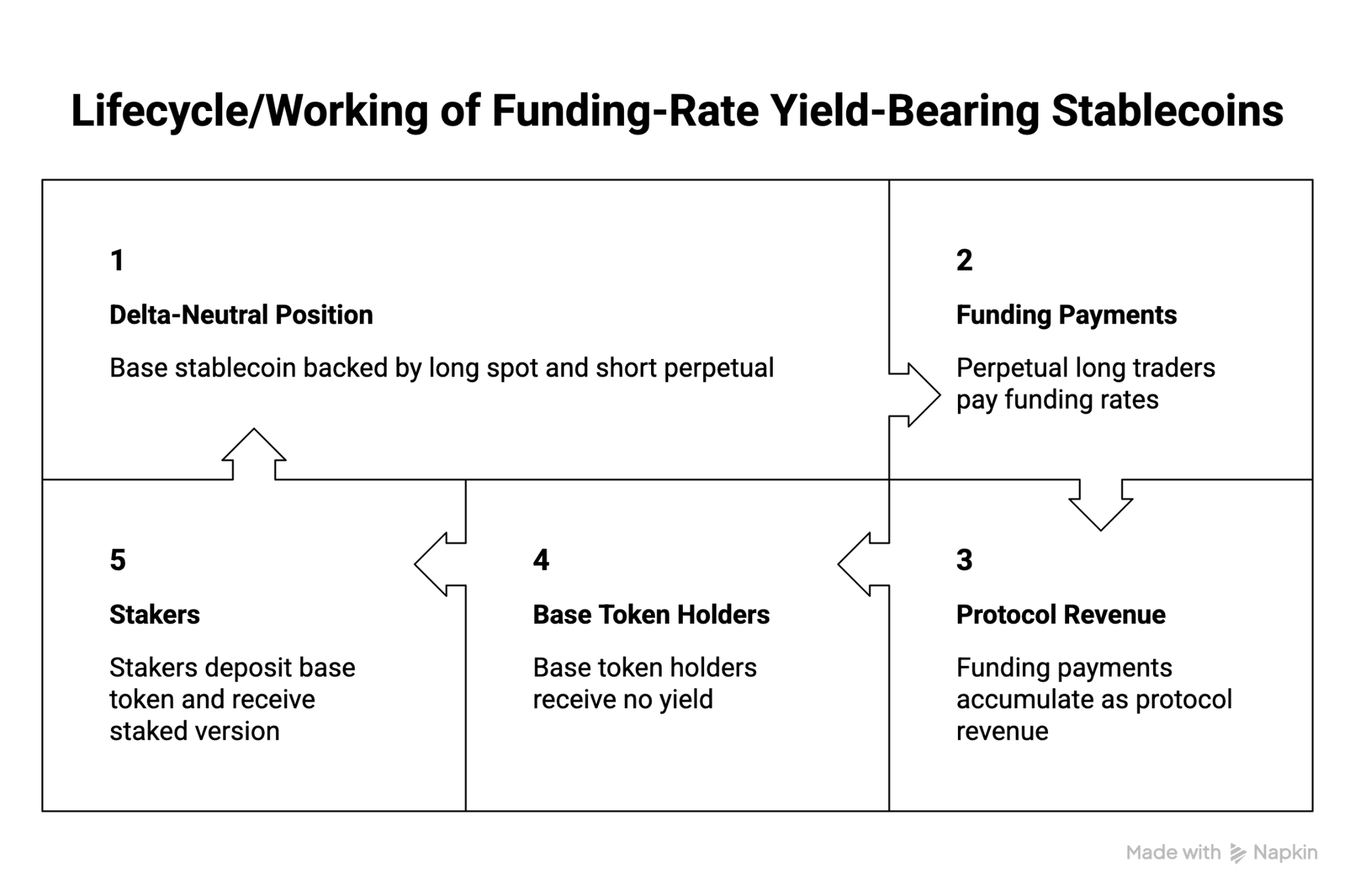

Funding-Rate Yield-Bearing Stablecoins

Funding-rate yield-bearing stablecoins generate returns by capturing payments from derivatives markets.

The most prominent example is Ethena's sUSDe, where funding received from perpetual futures markets is distributed to participants.

How do funding-rate yield-bearing stablecoins work?

Benefits of funding-rate yield-bearing stablecoins are:

- Generates crypto-native yield which is independent of traditional finance and runs 24/7.

- Funding rates are publicly observable across all major perpetual markets.

- Highly scalable through liquid derivatives venues.

Important to note: For all yield-bearing stablecoins, holders bear fund-level, custodian, and other risks. There are protocol-level buffers in place to accommodate downside before the retail participants get impacted.

Now that we have gone through all different types of stablecoins possible, what next? Is there a perfect stablecoin?

Final Insights: Is There a Perfect Stablecoin?

There is no perfect stablecoin. The question isn't whether one design is objectively better than another. It’s what stablecoin is trying to optimize for.

As stablecoins evolve from trading instruments into financial infrastructure, the market is unlikely to converge on a single winner.

Instead, it will fragment into specialized designs built for different users, jurisdictions, and use cases.

Regulation is drawing a clear line between payment stablecoins (licensed, yield-free, fiat or RWA-backed) and everything else. GENIUS and MiCA both bless the first category. The second — synthetic, CDP-minted, yield-bearing — keeps growing outside regulated venues anyway.

The market has decided it wants both: a compliant dollar for payments and a yield-generating dollar for DeFi.

The future of stablecoins is not one perfect digital dollar.

It is a spectrum of trade-offs, where the right design depends entirely on the purpose it is meant to serve.

FAQs: Frequently Asked Questions

- How do stablecoins maintain their peg?

Stablecoins maintain their peg through mechanisms such as reserve-backed redemption, overcollateralization and liquidations, derivatives hedging, commodity reserves, or income-generating real-world assets.

- What are the main types of stablecoins?

Stablecoins can be classified by collateral mechanism, issuance model, and yield model. By collateral mechanism, the main types are fiat-backed, crypto-collateralized, synthetic or delta-neutral, commodity-backed, and RWA-backed stablecoins.

- What is the difference between USDT and USDC?

Both are fiat-backed, but they differ in transparency, regulatory posture, and reserve composition.

- USDC is issued by Circle (NYSE-listed), holds reserves in a BlackRock-managed money market fund, and provides Deloitte attestations.

- USDT is issued by Tether (offshore), holds ~80% in T-bills with gold and Bitcoin comprising most of the remainder, and uses BDO attestations.

- Are stablecoins regulated?

Increasingly, but unevenly.

The GENIUS Act (US, signed July 2025) and MiCA (EU) both establish licensing requirements for fiat-backed payment stablecoins:

- mandating 1:1 reserves,

- monthly attestations, and

- prohibiting issuers from paying yield.

Offshore issuers and decentralized yield-bearing designs operate largely outside these frameworks

- Are all stablecoins backed by US dollars?

No. While many stablecoins target the US dollar, some are backed by crypto assets, commodities such as gold, or portfolios of real-world assets. The backing mechanism depends on the stablecoin's design.

- What is the safest type of stablecoin?

There is no universally safest stablecoin. Fiat-backed stablecoins generally offer the strongest peg stability and regulatory clarity, while crypto-native designs prioritize transparency, decentralization, or capital efficiency. The right choice depends on the risks you are willing to accept.

- Can one stablecoin fit into multiple categories?

Yes. A stablecoin can be classified across multiple dimensions at the same time.

For example, a stablecoin may be fiat-backed, issuer-minted, and Treasury yield-bearing.

- Why do stablecoins lose their peg?

Stablecoins typically lose their peg when the mechanisms supporting them fail. This can happen because of reserve shortfalls, failed liquidations, impaired hedging strategies, redemption constraints, or a loss of market confidence.

About Quicknode

Founded in 2017, Quicknode provides world-class blockchain infrastructure to developers and enterprises. With 99.99% uptime, support for 80+ blockchains, and performance trusted by industry leaders, we empower builders to deploy and scale next-generation applications across Web3.

Start building today at Quicknode.com.