Tokenized Equities 2026: Inside the Future of Global Equity Markets

Tokenized equities are stocks and ETFs issued on blockchains. Here's what they are, how they work, and what's still broken.

Tokenized equities are already trading, settling, and being used as collateral onchain. But what’s being traded is not always the same thing.

Everything from a legal share to a fund unit, a custodial claim, or even a derivative is being umbrella-d into ‘tokenized equities’ and it paints a very misleading picture.

So, we decided to break it all down and cover everything that matters.

This piece explains tokenized equities, the different architectures, the actual value unlocks, the risks, and leading players in the market.

What Are Tokenized Equities

Tokenized equities are digital representations of publicly listed stocks and ETFs, issued and transferred on a blockchain.

They track the price of the underlying asset and allow investors to trade, hold, and transfer equity exposure onchain with 24/7 settlement and regulatory compliance.

Sounds simple, right? Let’s now understand how all of these actually operate.

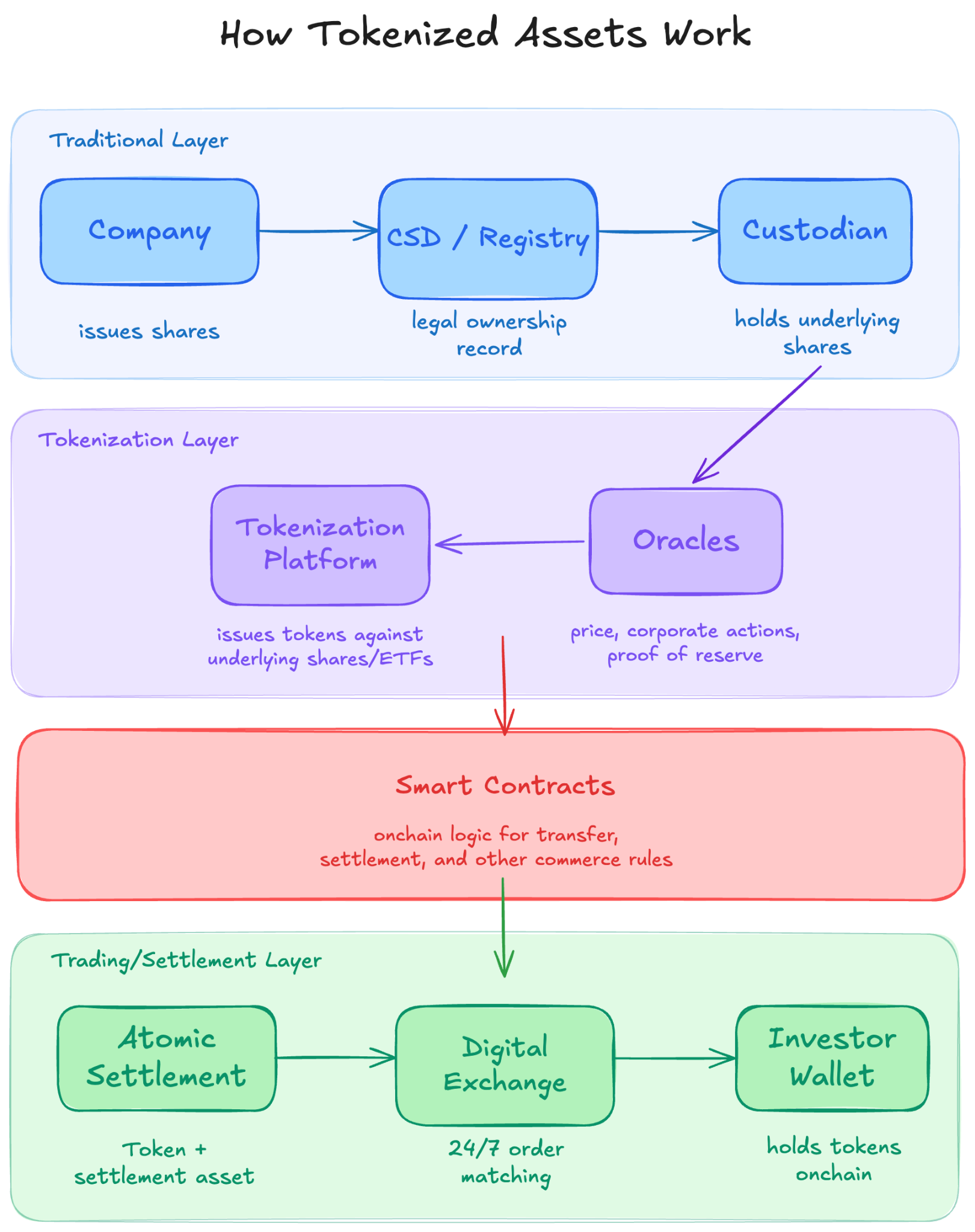

How Tokenized Equities Work

Tokenized equities connect two very different systems: traditional capital markets where assets originate, and blockchains where they move and settle.

The flow below shows how an equity moves from issuance to custody, gets represented onchain, and is ultimately traded and settled.

At its core, tokenizing an equity means rebuilding three layers of traditional market infrastructure — issuance, compliance, and settlement — on a blockchain.

The infrastructure and process is now clear. But, since tokenized equities aren’t standardized, there are a few different types that are live.

The Four Architectures of Tokenized Equities

Not all tokenized equities represent the same thing or carry the same legal weight.

While they may look identical onchain, they are built on different structures that define what you actually own, how it’s enforced, and where the risks sit.

Here’s a quick table comparing four common architectures of tokenized equities:

Despite all of them operating under the same asset title 'tokenized equities', each of the above are unique in how the investor has economic exposure.

This is important since it determines everything downstream:

- regulatory treatment,

- consequences during corporate actions (voting, dividends, etc),

- priority during claims, and

- composability within the DeFi ecosystem.

Having learnt what tokenized equities are, how they work, and what investors actually own, let's dive into the market and leading players.

Tokenized Equities Market: Overview of the Leading Players

The tokenized equities market has a handful of serious players.

Each issue tokens tied to publicly listed stocks or ETFs and allows holders to gain equity exposure onchain.

Where they differ is in legal structure, regulatory standing, geographic reach, and how deep into DeFi composability they go.

Securitize

Securitize with its “Tokenize the World” tagline is arguably the most institutionally aligned player in the space and currently serves over $4B+ in tokenized assets.

Its primary products are tokenized fund interests like BlackRock BUIDL, Apollo ACRED, VanEck VBILL.

How Securitize works

Securitize operates as a regulated transfer agent and broker-dealer, issuing tokenized securities through its DS* Protocol v4.

The real assets sit offchain with custodians like BNY Mellon and Securitize acts as the SEC-registered transfer agent by,

- Minting/burning blockchain tokens that represent shares,

- Enforces compliance at wallet-level, and

- Automating settlements and payouts.

Securitize investors, primarily, receive shares in tokenized funds and not direct equities.

Access to Securitize is strictly permissioned. Most offerings are structured under exemptions like Regulation D and Regulation S, which means:

- Investors must be accredited or qualified purchasers (ex: $5M+ investable assets for products like BUIDL)

- Participation is restricted by jurisdiction (ex: separate rules for US vs non-US investors)

- Only KYC-verified investors with pre-whitelisted wallets can buy, hold, or transfer tokens.

Securitize stands out as the deepest regulatory stack in the market:

- SEC-registered transfer agent

- Broker-dealer and ATS capabilities

- Fund administration and EU investment firm licenses

However, all of the above permissioned tangents make Securitize a highly concentrated and non-retail protocol with no direct equity offerings.

Ondo Finance (Global Markets)

Ondo GM is a tokenization platform that allows non-US investors to directly access 200+ tokenized US stocks and ETFs including AAPL and TSLA.

‘Onchain stock, wallstreet liquidity’ represents what Ondo does and enables fittingly.

How Ondo works

- Ondo issues tokenized stocks (TSLAon) as a 1:1 mirror for the Tesla (TSLA) stock.

- Underlying shares are purchased and held by Alpaca Securities, a US-registered broker-dealer and custodian.

- Tokens are issued against these holdings, representing a secured contractual claim on the SPV.

- Price and corporate data are fed onchain via Chainlink Data Streams.

- Tokens are deployed across Ethereum, Solana, and BNB Chain, with cross-chain transfers enabled through LayerZero.

Also, please note: Ondo Global Markets work 24 hours but only for 5 days from Sunday 8 pm ET to Friday 7 pm ET.

What Ondo offers investors

Users when they buy a tokenized stock on Ondo technically receive a secured contractual claim against the SPV plus economic exposure to total return.

Dividends earned on these stocks are reinvested automatically minus ~30% US withholding tax.

Access to Ondo is restricted to non-US investors under Regulation S. In detail,

- Users in the US, UK, Canada, and several other jurisdictions are blocked

- KYC is required at onboarding

- Once issued, tokens can be held and transferred onchain in self-custody

Ondo also received Liechtenstein FMA approval, allowing passporting across ~30 EEA countries for professional investors.

Ondo stands out in scale and onchain integration:

- ~$600M+ in tokenized equities TVL

- $9B+ cumulative trading volume since launch (Sept 2025)

- Accepted as collateral across Morpho, Euler, and 1inch

- Ondo Global Listing, launched in February 2026, enables same-day tokenization of IPOs.

Ondo delivers one of the cleanest user experiences for tokenized equities today but the trade-offs of single custody and dividend drag needs to be accounted for.

Superstate

Superstate is a regulated onchain asset manager best known for its tokenized Treasury fund USTB.

But for tokenized equities, their new initiative, ‘Opening Bell’ which is a native equity issuance platform is more relevant.

How Opening Bell works

Opening Bell is the only platform in this market where the token is the actual SEC-registered share officially registered onchain.

- The token is the legal share. They’re issued as SPL on Solana or ERC-20 on Ethereum.

- Cap table updates are recorded onchain via a registered transfer agent.

- Issuance, transfers, and ownership updates happen through onchain transactions tied to regulated entities.

What Opening Bell investors get is direct equity of a full SEC-registered common stock with voting rights, dividend entitlement, and legal rights.

More importantly, there is no SPV holding the underlying or any intermediary between the token and the share.

Access to Superstate is permissioned and allowlist-based:

- Investors must complete KYC/AML onboarding

- Wallets are whitelisted before they can hold or transfer shares

- Transfers are restricted to approved participants

Where Superstate stands out is in being the only native-issuance model in live production.

Their Direct Issuance Program further allows public companies to issue new tokenized shares directly onchain for stablecoins with real-time cap table update.

For now, Superstate is the most complete and legally defensible tokenized equities design. A truer picture will likely show up as more users, issuers, liquidity, and use cases get onboard.

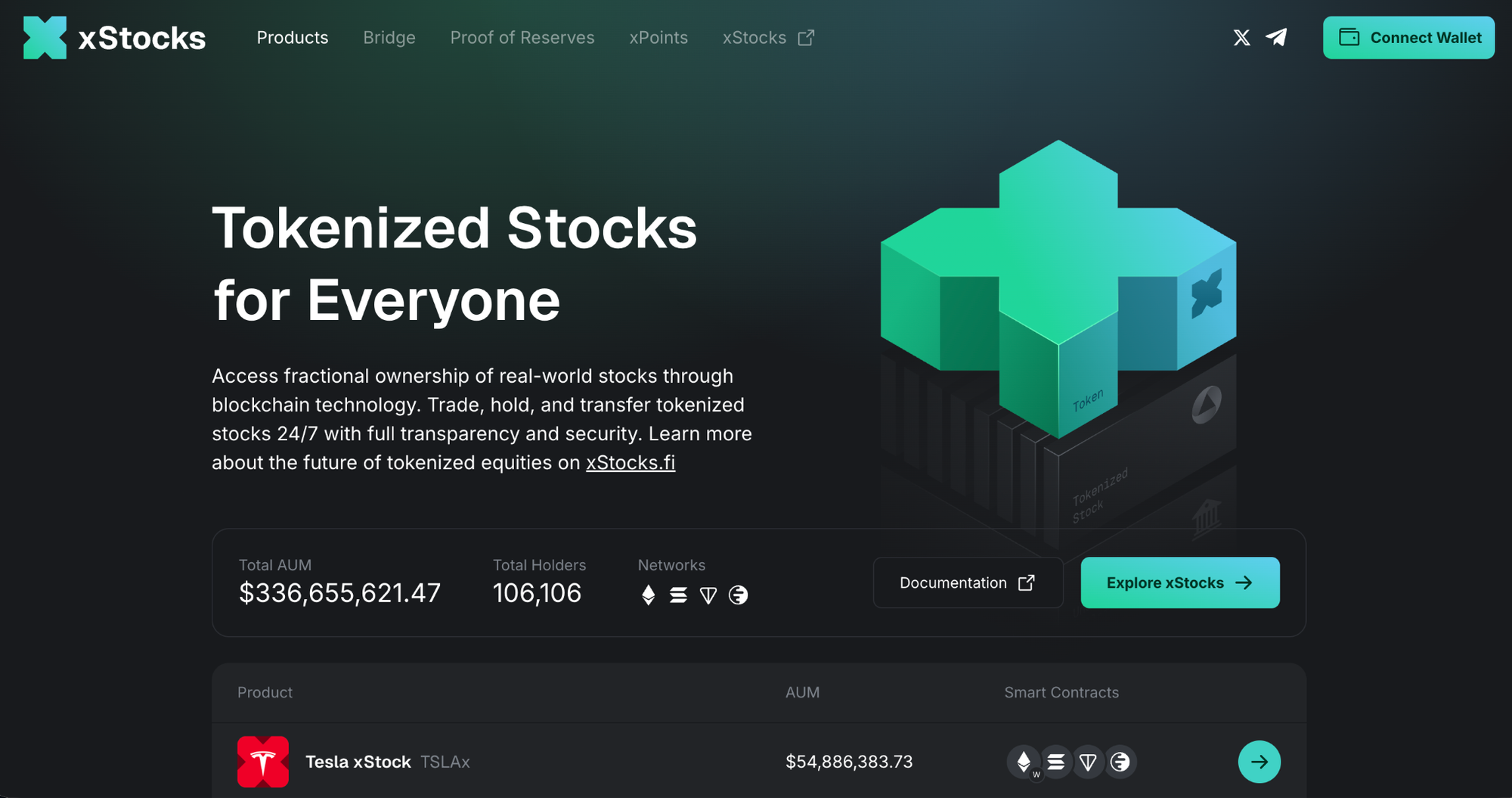

xStocks

xStocks (a Backed product) is the most widely distributed tokenized equity product in the market.

Since launching in June 2025, xStocks has crossed $25B in cumulative transaction volume.

How xStocks works

xStocks are issued by Backed Assets (JE) Limited, a Jersey-based SPV, under a Liechtenstein FMA-approved prospectus.

- Each xStock represents a tracker certificate (a debt instrument) in the form of a SPL token on Solana or similar on Ethereum.

- Underlying shares are purchased and held 1:1 by Alpaca Securities against which xStocks are minted.

- Chainlink Proof of Reserve publishes weekly verification, backed by quarterly ISAE 3000 assurance audits.

xStocks operates 24/5 across Solana, Ethereum, and other blockchains.

What xStocks investors get is economic exposure to price movements of the underlying stock or ETF.

Dividends, like in the case of Ondo, are reinvested minus 30% withholding tax.

Access to xStocks is available globally excluding the US, under the Liechtenstein regulatory framework.

KYC is enforced at the distributor level i.e. platforms like Kraken, Bybit, Gate.io, KuCoin.

Where xStocks stands out is scale and distribution: Already, 100+ xStocks are live with 100K + holders.

All the trade-offs are borrowed from the instrument type in itself. As a credit instrument, there's a dependence on custodians (Alpaca) and issuer structure.

xStocks is the most accessible and liquid implementation in the market today.

Dinari

Dinari is the most US-native attempt at tokenized equities. It is the first SEC-registered broker-dealer approved to tokenize securities.

How Dinari works

Dinari operates as an SEC-registered broker-dealer and transfer agent, issuing tokenized equities (“dShares”) backed 1:1 by real shares.

- A KYC-verified user deposits USDC, USDT, or USD+.

- Dinari routes the order to Alpaca, which purchases and custodies the underlying share on a US exchange.

- Dinari mints the equivalent dShare to the user's wallet onchain.

- LayerZero OFT enables cross-chain transfers across four blockchain with Solana deployment coming soon.

The core difference between other tokenized models and Dinari is that with Dinari, issuance and custody sit within US regulatory rails.

What Dinari offers investors is a 1:1 economic exposure to the underlying security.

This is where dShares needs to be deconstructed carefully:

- dShares are a tokenized fully-funded OTC derivative.

- They are a fully-funded, unleveraged contract linked 1:1 to the performance of the underlying stock/ETF.

- So, investors don't own the equity but only have a claim against Dinari for their OTC derivative.

Dividends are paid in USD+ which is Dinari's own yield-bearing stablecoin backed 1:1 by US Treasuries.

Access to Dinari is global and KYC-gated. European distribution runs through the Gemini EU platform. However, there's no active US retail access yet.

Where Dinari stands out is with its US-first positioning.

It has all the onshore approvals required to meet existing securities law which is a key headstart no other platform has.

Dinari is building toward a version of tokenized equities that can operate inside US markets but today, the ecosystem around it is still early and thin.

Now, let’s move ahead. Now, the question is simple:

If every implementation makes different trade-offs, what does tokenization actually unlock that traditional equities cannot?

Making the Case for Tokenized Equities: What Actually is the Unlock?

Tokenized equities are often reduced to two benefits: 24/7 trading and global access.

Outside these, let’s learn more about four non-obvious but consequential unlocks:

Atomic settlement eliminates counterparty exposure

In traditional markets, the period between trade execution and settlement is a credit risk window. T+1 means a counterparty can fail before finality.

Atomic DvP collapses that window to zero. The token and the payment asset exchange hands in a single transaction, or neither does.

Composability is a major unlock

A tokenized share sitting in a wallet is doing nothing.

The same share posted as collateral on Kamino or Morpho earns yield against a loan without,

- custody transfer,

- rehypothecation complexity, or

- any intermediary.

This capital efficiency implication:equity that simultaneously earns returns and backs borrowing has no traditional market peer.

Programmable compliance

In traditional markets, compliance is enforced at the intermediary level like brokers, custodians, or clearinghouses.

Tokenized equities encode compliance rules into smart contracts.

Transfer restrictions, accreditation checks, jurisdiction blocks, and investor limits can be executed automatically at the token level on every transaction.

Corporate actions become programmable flows

Similar to above, corporate actions like dividends, splits, and rights issues don’t need manual coordination across brokers, custodians, and registries.

They can be originated, validated, and executed as onchain state transitions, reducing reconciliation risk and latency.

Tokenized equities are changing how equity capital is held, moved, and deployed. The upside is clear.

But every one of these unlocks introduces new dependencies and new risks.

Critical Gaps in Tokenized Equities

The capabilities of tokenized equities are real. But, there are 3 structural gaps to address before any of these capabilities can come to live.

The first major one is all related to liquidity.

Liquidity Risks

Tokenized equities are often discussed as a single market. They are not.

The same underlying asset — say, a tokenized Apple share — can exist across multiple chains, multiple issuers, and multiple platforms simultaneously.

And each comes with their own liquidity pool, its own price, and no guaranteed arbitrage mechanism connecting them.

All of these are different forms of liquidity fragmentation and it can show up in a multitude of ways:

- Fragmented order books: Liquidity is split across venues (CEXs, onchain AMMs, RFQ systems), increasing slippage and weakening price discovery.

- Arbitrage dependency: Price alignment depends on arbitrageurs bridging gaps between venues and the underlying market.

When capital or access is constrained (jurisdictional limits, off-hours), these links weaken.

- Intraday liquidity gaps: Liquidity is not continuous.

Even if trading is “always on”, depth can disappear outside peak hours, leading to sharp price impact on relatively small trades.

- Exit risk under stress: In volatile conditions, redemptions, spreads, and liquidity can break simultaneously.

Liquidity’s deeper issue is structural: each new chain deployment adds an isolated pool without automatically deepening any of the others.

Until cross-platform liquidity is unified — technically, legally, and operationally — the market remains a collection of thin venues rather than one deep one.

Apart from liquidity, there are a few other hiccups that tokenization platforms need to address.

Custodian and Intermediaries Paradox

The tokenization promise is direct ownership without needing intermediaries that cause operational friction or a custody chain that adds risk and cost.

Yet, all the tokenized equities models we have covered depend on custodians: SPVs or funds, clearing brokers, oracle operators, admin key holders.

These new intermediaries are less regulated, less capitalized, and less battle-tested than the ones they replace which is riskier for the investor.

Stress Propagation

Because these systems are layered (custodian > issuer > token > DeFi), failures cascade.

A custody issue, oracle lag, or redemption pause can quickly spill into pricing dislocations, automated liquidations, or collateral stress across protocols.

Since these workflows are more automated and have less human intervention, there are a lot of edge cases related to risks and recourse that will be tested for the first time.

So, what’s the future of tokenized equities looking like?

The Future of Tokenized Equities

Tokenized equities work technically.

Shares settle atomically. Dividends reach wallets in stablecoins. Collateral positions open against equity without a prime broker.

All of these are in production today.

Across everything covered — architectures, players, liquidity, custody, and execution — the same pattern shows up:

- Onchain systems are fast, programmable, and composable.

- Offchain systems are legal, enforced, and authoritative.

Today, tokenized equities sit between the two.

What the market needs is not just regulatory clarity. It is regulatory architecture where legal ownership, transfer mechanics, corporate action obligations, and investor protections are defined for onchain and tokenized instruments specifically.

Until then, tokenized equities will continue to exist as hybrid systems: powerful, but limited.

About Quicknode

Founded in 2017, Quicknode provides world-class blockchain infrastructure to developers and enterprises. With 99.99% uptime, support for 80+ blockchains, and performance trusted by industry leaders, we empower builders to deploy and scale next-generation applications across Web3.

Start building today at Quicknode.com.